How to Complete the FAFSA: A Guide for Students and Families

The Free Application for Federal Student Aid (FAFSA) is how students access federal grants, work-study, and loans for college. Whether you're planning for college in high school or renewing aid as a current student, understanding when to apply, who needs to complete it, and what information you'll need is essential for maximizing your financial aid eligibility.

Who This Guide Is For

Seniors applying to college, current college students renewing financial aid, parents and contributors helping with the application, and anyone seeking federal or state financial assistance for education.

Who Needs to Complete the FAFSA?

Any student planning to attend college, community college, trade school, or career school should complete the FAFSA—regardless of family income. FAFSA determines eligibility for federal, state, institutional, and private financial assistance.

Students Who Must Apply

- • Seniors entering college for the first time

- • Current college students who need aid for the upcoming academic year

- • Graduate students seeking loans or other federal aid

- • Transfer students changing schools who need continued aid

- • Part-time students attending less than full-time

- • Trade and technical school students in eligible programs

Who Serves as a Contributor

Contributors are individuals required to provide information and consent on the FAFSA. Each contributor must create their own FSA ID.

- → The student (always required)

- → Student's spouse (if married)

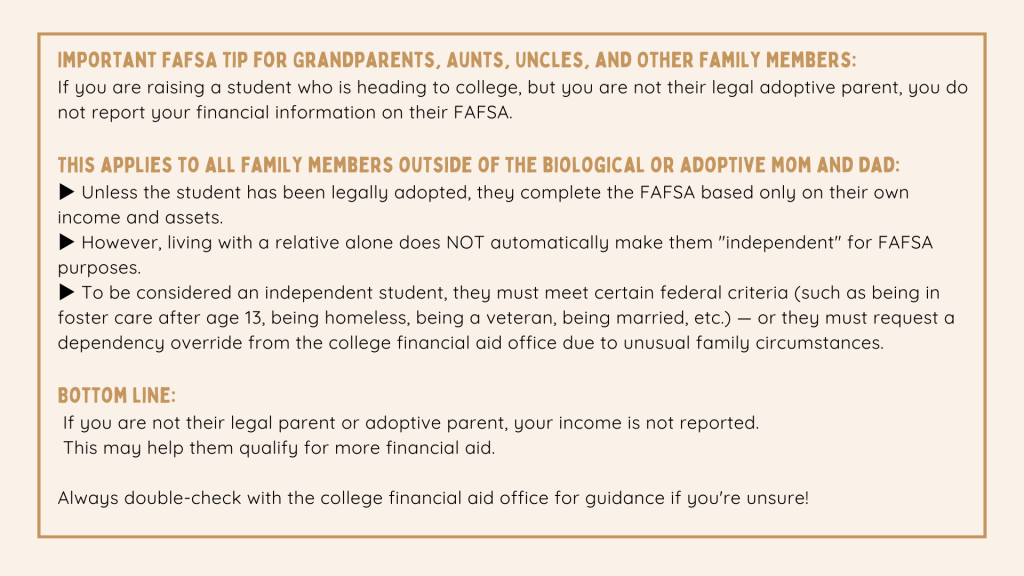

- → Biological or adoptive parent(s) (for dependent students)

- → Stepparent (if married to the custodial parent)

Important: Even if you think your family earns "too much" for financial aid, you should still apply. Many scholarships and institutional aid programs require FAFSA completion regardless of need.

When to Apply and Renewal Requirements

Understanding FAFSA deadlines and renewal requirements is critical for maintaining continuous financial aid eligibility. Missing deadlines can cost you thousands of dollars in grants and aid.

FAFSA Application Window

When the FAFSA Opens:

The FAFSA form opens every year on October 1st for the following academic year.

Priority Deadlines:

Many states and colleges have priority deadlines as early as November or December. Submit as soon as possible after October 1st to maximize aid eligibility.

Best Practice:

Complete your FAFSA in October or November of your senior year to meet early deadlines and secure the most aid.

Annual FAFSA Renewal

How Often to Apply:

You must complete a new FAFSA every single year that you need financial aid. This applies to all students—freshmen, sophomores, juniors, seniors, and graduate students.

Why Annual Renewal is Required:

Your family's financial situation may change from year to year. Federal aid eligibility is recalculated annually based on updated income and tax information.

What Happens If You Don't Renew:

Your financial aid will stop. You won't receive grants, work-study, or federal loans for the upcoming year.

Don't Wait: Many state grants and institutional aid programs operate on a first-come, first-served basis. Students who submit early receive more aid than those who wait until spring.

Texas FAFSA Deadlines

Texas students should be aware of state-specific deadlines for maximum financial aid eligibility:

TEXAS Grant Priority Deadline: January 15th

The Towards EXcellence, Access, & Success (TEXAS) Grant provides aid to students with financial need attending Texas public universities. Submit your FAFSA by January 15th for priority consideration.

Texas College Work-Study Deadline: Varies by School

Texas College Work-Study Program deadlines vary by institution. Check with your school's financial aid office for specific dates, but plan to submit by December or January for best availability.

Community College Grants: Rolling Basis

Texas community colleges distribute state and institutional aid on a rolling, first-come first-served basis. Submit as early as possible after October 1st.

Best Practice for Texas Students: Submit your FAFSA by mid-December to meet most Texas state aid priority deadlines and maximize your eligibility for state grants and work-study programs.

How to Complete the FAFSA: Step-by-Step Timeline

Follow this step-by-step timeline to successfully complete your FAFSA and secure your financial aid package. Each step is important for maximizing your eligibility and meeting critical deadlines.

Create FSA IDs (Start Early)

Every contributor must create their own FSA ID at StudentAid.gov. This username and password will be used to access, sign, and submit the FAFSA. FSA IDs are now active immediately upon creation.

Who Are Contributors?

Contributors are the people required to provide information and consent on the FAFSA:

- • The student (always required)

- • Student's biological or adoptive parent(s) (for dependent students)

- • Student's stepparent (if married to the custodial parent)

- • Student's spouse (if the student is married)

What Contributors Need to Do:

Each contributor must create their own FSA ID, provide consent for federal tax information to be transferred directly from the IRS, answer questions about their income and assets, and electronically sign the FAFSA using their FSA ID.

Contributors Without Social Security Numbers:

Contributors who don't have a Social Security Number (SSN) can still create an FSA ID and complete their portion of the FAFSA. The FAFSA system accommodates all contributors regardless of citizenship or immigration status. However, the student's eligibility for federal aid depends on their own citizenship status, not that of their parents or contributors.

Timeline: September - Early October (before FAFSA opens)

Gather Required Documents

Collect Social Security numbers, driver's license numbers, tax returns (previous year), W-2 forms, records of untaxed income, bank statements, and investment records for student and parents/contributors.

Timeline: September - Early October

Complete and Submit FAFSA (Opens October 1st)

Log in to StudentAid.gov, start a new FAFSA form for the correct academic year, provide student and family information, list schools you're applying to, and have all contributors provide consent and sign electronically with their FSA IDs.

Timeline: October 1st - November (submit early for priority deadlines)

Review Your Student Aid Report (SAR)

Within 3-5 days of submitting, you'll receive a Student Aid Report summarizing your FAFSA information. Review it carefully for errors and make corrections immediately if needed. Your Expected Family Contribution (EFC) or Student Aid Index (SAI) will be included.

Timeline: 3-5 days after FAFSA submission

Schools Receive Your FAFSA Information

The schools you listed on your FAFSA will automatically receive your information and begin calculating your financial aid package. Some schools may request additional verification documents or have their own financial aid forms to complete.

Timeline: Within 1-2 weeks of FAFSA submission

Receive Financial Aid Award Letters

Each college will send you a financial aid award letter detailing your aid package, including grants, Scholarships, work-study, and loans offered. Compare packages from different schools carefully, considering net cost and types of aid offered.

Timeline: Late winter to early spring (varies by school)

Accept or Decline Aid and Complete Additional Requirements

Review your aid package and accept or decline each component by the school's deadline. For federal student loans, complete entrance counseling and sign a Master Promissory Note. Submit any required verification documents to your school's financial aid office.

Timeline: Spring (typically by May 1st college decision deadline)

Aid Disbursement and Enrollment

Your financial aid will be applied directly to your student account for tuition, fees, and on-campus housing. Any remaining funds will be refunded to you for other education expenses like books, supplies, and off-campus living costs. Aid typically disburses at the beginning of each semester.

Timeline: Before and during each semester

Remember: You must complete a new FAFSA every year. Set a reminder to renew your FAFSA each October for continuous financial aid throughout college.

Understanding Your Financial Aid Options

The FAFSA is your gateway to federal grants, work-study, and student loans. States, colleges, and private Scholarships providers also use your FAFSA information to determine additional aid eligibility.

Grants & Scholarships

Free money that doesn't require repayment. Grants are typically need-based, while scholarships reward achievement or other criteria.

Part-time employment program that lets you earn money for education while gaining work experience. Jobs have flexible hours around your class schedule, with earnings paid directly to you.

Federal Student Loans

Money that must be repaid with interest. Features fixed interest rates and flexible repayment options. Borrow only what is necessary for your education.

State & Institutional Aid

Many states and colleges use FAFSA to determine their own aid programs and scholarships. Apply early for best results.

Understanding Federal Loan Types

Federal student loans come in two main types: subsidized and unsubsidized. Understanding the differences helps you make smarter borrowing decisions and minimize long-term debt.

Subsidized Loans

- ✓ No interest during school – Interest doesn't accrue while you're enrolled at least half-time

- ✓ Based on financial need – Eligibility determined by your FAFSA results

- ✓ Lower borrowing limits – $3,500-$5,500 per year depending on grade level

- ✓ Government pays interest until repayment – Also during grace period and deferment

- ✓ Better long-term cost – Can save thousands in interest over the life of the loan

Unsubsidized Loans

- • Interest accrues immediately – Starts accumulating from disbursement date

- • Not based on financial need – Available to all students regardless of income

- • Higher borrowing limits – $5,500-$20,500 per year depending on grade level and dependency

- • You're responsible for all interest – Can pay interest while in school or let it capitalize

- • Higher long-term cost – Interest adds to principal balance if not paid during school

Loan Borrowing Strategy

Always accept subsidized loans first (if offered), then evaluate unsubsidized loans only if needed. Subsidized loans save you money because the government pays the interest while you're in school.

Consider the 4-year total: Borrowing $5,000/year = $20,000+ with interest by graduation. Calculate the total cost over all years of school, not just one semester, to understand your true debt burden.

Special Circumstances and Professional Judgment Appeals

If your family has experienced a significant change in financial circumstances that impacts your ability to pay for college, you can request a professional judgment review from your school's financial aid office. Financial aid officers have the authority to make adjustments to your FAFSA information based on special circumstances.

Qualifying Special Circumstances

↓Employment Changes

- • Job loss or layoff after filing FAFSA

- • Significant reduction in work hours or income

- • Loss of benefits (child support, unemployment, etc.)

- • Retirement or disability preventing work

Family Structure Changes

- • Death of a parent or spouse

- • Divorce or separation of parents

- • Change in household size (new dependents)

- • Change in marital status of student or parent

Medical & Emergency Expenses

- • Significant unreimbursed medical or dental bills

- • Prescription medication costs not covered by insurance

- • Expenses for care of ill or elderly family members

- • Natural disaster or emergency situation losses

Other Financial Hardships

- • Elementary or secondary school tuition for siblings

- • Unusually high dependent care costs

- • Loss of untaxed income or benefits

- • One-time income that won't recur (inheritance, bonus)

How to Request a Professional Judgment Review

↓Step 1: Contact the Financial Aid Office

Reach out to the financial aid office at each school where you've been accepted. Ask specifically about their "special circumstances appeal" or "professional judgment review" process. Many schools have a specific form to complete.

Step 2: Gather Documentation

Collect official documentation that proves your special circumstances. Financial aid offices require third-party verification and cannot accept verbal explanations alone.

Examples of Required Documentation:

- • Layoff notice or termination letter from employer

- • Unemployment benefit statements

- • Death certificate

- • Divorce decree or separation agreement

- • Medical bills and insurance statements showing out-of-pocket costs

- • IRS tax transcripts showing current year income

- • Recent pay stubs showing reduced income

Step 3: Write a Detailed Letter of Explanation

Compose a formal letter explaining your circumstances, when they occurred, and how they impact your ability to pay for college. Be specific about dollar amounts and timeframes.

Include: Your name and student ID, specific circumstances, date the change occurred, financial impact (exact dollar amounts), supporting documentation list, and a clear request for reconsideration of your aid package.

Step 4: Submit and Follow Up

Submit all documentation by the school's deadline (often 2-4 weeks before the semester starts). Follow up within one week to confirm receipt, and be prepared to provide additional documentation if requested. Decisions typically take 2-3 weeks.

Important: Professional judgment reviews are decided on a case-by-case basis and are not guaranteed. However, schools genuinely want to help students overcome financial barriers. Be thorough, honest, and persistent in your appeal. Don't hesitate to advocate for yourself and your family.

Scholarships: Additional Financial Aid for College

While FAFSA opens the door to federal and state financial aid, Scholarships provide additional funding that doesn't need to be repaid. Many Scholarships have deadlines between October and March, so start your search early.

Scholarships reward academic achievement, leadership, community service, talents, and many other criteria. Some require FAFSA completion, while others have separate applications.

Tips for Scholarship Success

- • Start searching for scholarships during junior year and continue through senior year

- • Apply to multiple scholarships to increase your chances of receiving aid

- • Pay attention to deadlines and required materials for each scholarship

- • Look for local scholarships with less competition in addition to national opportunities

Frequently Asked Questions

Do I need to complete FAFSA every year?

↓Yes, you must complete a new FAFSA application every single year that you need financial aid. Your financial aid eligibility is recalculated annually based on updated family income and tax information. If you don't renew, your aid will stop—even if you received federal grants or loans in previous years.

When should I submit my FAFSA?

↓Submit your FAFSA as soon as possible after it opens on October 1st each year. While the federal deadline isn't until June, many states and colleges have priority deadlines as early as November or December. Submitting early maximizes your eligibility for grants and aid that operate on a first-come, first-served basis.

What is an FSA ID and who needs one?

↓An FSA ID is your personal login for StudentAid.gov, consisting of a username and password. Every contributor on the FAFSA needs their own FSA ID—including the student, parents (for dependent students), stepparents (if married to the custodial parent), and spouses (for married students). Without an FSA ID, contributors cannot complete their portion of the FAFSA.

Should I apply even if my family has high income?

↓Yes, absolutely. Many Scholarships and institutional aid programs require FAFSA completion regardless of need. Additionally, all students qualify for unsubsidized federal loans regardless of family income, and these often have better terms than private loans. Some colleges also use FAFSA information for merit-based aid decisions.

Can contributors without Social Security Numbers complete the FAFSA?

↓Yes. Contributors who don't have a Social Security Number can still create an FSA ID and complete their portion of the FAFSA. The FAFSA system accommodates contributors regardless of citizenship or immigration status, though the student's eligibility for federal aid depends on their own citizenship status.

What types of financial aid does FAFSA determine eligibility for?

↓The FAFSA determines eligibility for federal grants (like Pell Grants), federal work-study programs, federal student loans (subsidized and unsubsidized), and serves as the basis for many state grants and institutional aid programs. Many private Scholarships providers also use FAFSA information to evaluate applicants.

What happens if I miss a payment deadline?

↓Late payment can result in late fees, holds on course registration, inability to access transcripts, and removal from housing. Most colleges offer payment plans that break tuition into monthly installments—enroll early to avoid issues. If you're facing financial difficulty, contact your school's bursar or financial aid office immediately to discuss options like emergency aid, short-term loans, or adjusted payment schedules.

Ready to Build Your Post-Secondary Candidacy?

Completing the FAFSA is just one step in building a strong candidacy for post-secondary success. A planning session can help you navigate financial aid, explore college options, and develop a comprehensive strategy that maximizes your opportunities. Schedule a session today to gain clarity on your path forward.

Schedule a Planning Session to Build Candidacy